For customers, paying with a credit or debit card can be as simple as a tap and a ‘beep’ during checkout — or inputting their details online. But within that split second of making a payment, there are several underlying technical processes that ensure businesses can operate efficiently.

The good news for business owners is that understanding payment processing doesn’t need to be complicated.

In this article, we’ll break down the key steps and options for payment processing and explain how it can impact your business. With our help, you can accept transactions with confidence.

In this guide:

What is payment processing?

Payment processing is the system that allows businesses to accept electronic payments, including debit and credit card transactions. This includes everything from processing a card and opening secure gateways, to communicating with issuing banks and consumer accounts.

Payment processing consists of two main parts.

- A payment gateway that securely transmits a customer’s payment information to financial institutions.

- A payment processor or ‘vendor’ that transfers money from the customer to the merchant.

What types of payment methods does payment processing support?

Some of the different types of payments that are processed include:

- Debit and credit cards — physical cards issued by banks’ permit holders, to borrow funds in exchange for products or services.

- Digital wallets — software applications, typically on mobile devices, that allow for electronic financial transactions.

- Bank transfers — electronic fund transfers that typically occur between businesses.

- Electronic checks — payment via paper checks converted into automated clearing house (ACH) transactions.

Why is payment processing important?

Payment processing allows for transactions to be quick and effective. Information is sent securely from merchant terminals to consumer banks, and back, in a matter of seconds.

These systems handle all communication between issuing banks, credit card networks, and financial institutions — and they do it without requiring the cashier or customer to understand or get involved in the process. This ensures a more streamlined customer journey and experience.

With ecommerce and digital transactions increasing, payment processing is no longer a helpful tool, but a necessity — especially when preparing a digital storefront for peak season.

- According to Deloitte’s trends and insights report for 2025, checks are gradually moving to extinction, and the use of cash is declining. Credit and debit card transactions, including peer-to-peer (P2P) transactions, will continue to grow in place of check payments.

- In the US, digital payments have now surpassed traditional payment methods, with 9 in 10 consumers reported to have made a digital payment in 2024.

How does payment processing work? A step-by-step guide.

Before exploring the different parts of payment processing, it’s important to understand the process.

Let’s look at the high-level steps required for payment processing and then dive deeper into its components.

- The customer initiates a transaction. A customer presents their card to a retailer, either in person or online.

- Payment data is passed through the payment gateway. The payment gateway transmits the cardholder's name, account number, and other card data securely.

- The payment gateway sends the data to the merchant’s bank. These details are then sent to the merchant’s bank.

- The payment processor notifies the issuer/the customer’s bank. The payment processor uses that information to notify the card’s issuing bank of the transaction.

- The issuer confirms or denies the purchase to the payment processor. Having been alerted of a transaction, the consumer’s bank confirms whether there are sufficient funds available for the transaction to take place. The transaction is either approved or declined.

- The transaction is recorded. When the payment is approved, the issuing bank lets the retailer know by communicating with the payment processor, and the transaction is recorded.

- The payment gateway notifies all involved. Every person involved, including the consumer and merchant, is notified via the payment gateway.

Payment gateways vs. payment processors.

Knowing the difference between payment gateways and payment processors is key to understanding how payment processing helps manage transactions efficiently. While both facilitate payments, they play differing roles in how funds move between a customer and a business.

What is a payment gateway?

Payment gateways serve as a link for all the entities involved with a transaction, and help different systems smoothly communicate with one another. Gateways come into play at the start and end of a card transaction.

A payment gateway makes it possible for banks — merchant and consumer — to communicate with one another to make a transaction. Specifically, payment gateways:

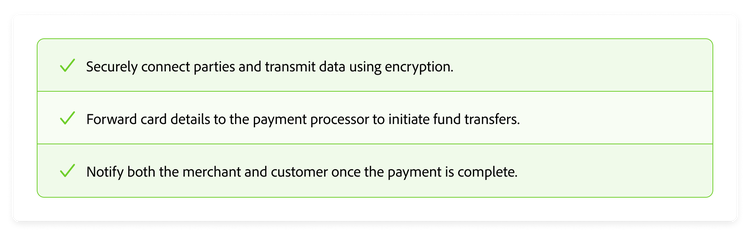

- Securely connect parties and transmit data using encryption.

- Forward card details to the payment processor to initiate fund transfers.

- Notify both the merchant and customer once the payment is complete.

Most card terminals and point-of-sale (POS) systems have payment gateways built into their structure to streamline the elements that your business needs to manage. In addition, there are payment processors that offer gateway options for use.

What is a payment processor?

If gateways are the components that connect banks, processors are the components that handle the actual logistics of those requests.

A payment processor is a system that allows for transactions to happen between consumer banks and merchants. As the name implies, it processes debit and credit card payments based on the requests it receives through the gateway.

Payment processors authenticate the transmitted information to confirm that it is valid with all the banks involved. The processor is responsible for the actual transfer of the funds, if approved, between the issuing bank (the consumer) and the merchant account (the retailer).

As a go-between for banks, consumers and merchants, payment processors come in many forms and are designed to handle transaction fulfilment.

They function as a business themselves, using several different models through which they charge merchants for their services:

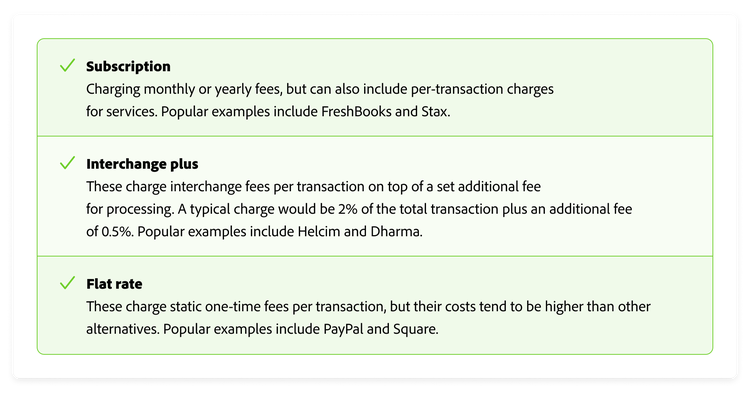

- Subscription. This model involves charging monthly or yearly fees but can also include per-transaction charges for services. Popular examples include FreshBooks and Stax.

- Interchange plus. These charge interchange fees per transaction on top of a set additional fee for processing. A typical charge would be 2% of the total transaction plus an additional fee of 0.5%. Popular examples include Helcim and Dharma.

- Flat rate. These charge static one-time fees per transaction, but their costs tend to be higher than other alternatives. Popular examples include PayPal and Square.

How to choose a payment processor.

The type of payment processor you choose should depend on your sales volume, where your transactions take place, and the products or services you offer.

Some payment processors are better suited to handling certain types of transactions, such as mobile payments. Others offer capabilities that are necessary for specific businesses; for example, allowing your customers to enter their credit card numbers manually.

Think about the steps your customers need to take to complete a purchase and then determine the features you need from your payment processor.

1. Review your pricing plans.

The right payment processor should also be cost-effective. The cost to process each payment is small but can add up, especially if your business deals with many purchases each day. When evaluating payment processors for your business, consider which fee structure is the best deal. The right pricing model for you will depend on how you operate.

- If you’re a small brick-and-mortar business that occasionally sells items online, a tiered pricing structure can get you the lowest rates associated with in-person sales.

- If you’re a large business with a profitable ecommerce store, an interchange-plus pricing scheme could be a cost-effective solution.

You’ll also want to determine if a payment processor will charge fees for your subscription, or any equipment provided.

Interchange-plus.

The plus in interchange-plus refers to an additional fee that payment processors charge on top of the interchange fee. The additional fee covers the payment processor’s operations costs and provides them with a profit.

This amount is based on a fixed set of rates that may be applied to a transaction depending on the circumstances. The time the customer made the purchase, the card that was used, and whether the transaction was automated or not, are a few relevant factors. Premium credit cards are also typically more expensive to process than less exclusive ones.

Interchange fees are generally 1% to 3% of the overall transaction price. They also include a set dollar amount in cents for each transaction. The amount your business will pay for each transaction will vary with the interchange rate.

Flat-rate.

Flat-rate processing blends the variable interchange rate into one flat fee for all transactions. A flat-rate fee structure might add 2% of the purchase price plus an additional $0.10. Some businesses prefer flat-rate processing because it makes the fee easier to predict and simplifies revenue forecasting.

This simplified take on payment processing fees is ideal for smaller businesses and startups, which may not have the resources to apply a different interchange rate to every transaction. The downside is you typically won’t get the best possible rate for each type of debit or credit card payment you process, compared to an interchange-plus fee structure.

Tiered.

Tiered pricing, also known as bundled pricing, charges a fixed amount per transaction on different types of purchases. All transactions are classified into three tiers according to their risk — qualified, mid-qualified, and non-qualified — and assigned a corresponding fee.

Under a tiered payment processing system, an in-person debit card purchase may be categorized as a qualified transaction. This is a safe transaction that might warrant a processing fee as low as 1% of the total transaction plus $0.10.

However, a riskier online credit card purchase might be considered a non-qualified purchase. In this scenario, your business could be charged 3% of the total transaction fee plus $0.15.

2. Factor in the fees.

Fees can vary depending on the provider and the type of transactions you process.

Common charges to keep in mind include gateway fees for using a payment gateway, currency conversion fees for international transactions, and chargeback fees if a customer disputes a payment. Some processors also charge flat rates, while others have percentage-based fees.

3. Consider where you sell.

How and where you sell can have an impact on the fees you pay for payment processing.

If you have a physical store, in-person transactions using physical card terminals often have lower fees because they’re considered lower risk. On the other hand, digital online payments may have higher fees due to the high risk of online fraud and chargebacks.

Ensuring data security in payment processing.

Security in customer data management remains a crucial part of every step in the payment process. Many systems come equipped with encrypted gateways to prevent data from being interpreted if it is inadvertently accessed.

However, security is also to be implemented at other stages of the process — and with good cause. Costly data breaches can cause harm to a business and its reputation.

To avoid this, keep a couple of things in mind.

1. Find an EMV point-of-sale system.

EMV stands for Europay, Mastercard, and Visa, and refers to the microchips that are embedded in the front side of newer debit and credit cards — which the three companies created. These chips are designed to help protect against fraud, since they can only be interpreted by specialized readers, limiting pathways for theft and data fraud.

2. Familiarize yourself with the Payment Card Industry Data Security Standard (PCI-DSS).

Businesses can also take time to understand the Payment Card Industry Data Security Standard, or ‘PCI-DSS’. This information security standard is often required of merchants for them to conduct debit and credit card payment processing, guaranteeing a minimum level of security.

These guidelines help inform which data should and should not be retained by a retailer during and after a transaction. Be sure to read the complete PCI-DSS and current requirements for more information.

3. Provide ongoing security and data training to employees.

Regular security and data training for employees involved in payment processing is essential for protecting both the business and its customers from fraud and data breaches.

Payment processing systems handle sensitive customer data and financial information, so your employees must stay informed on best practices to safeguard this data.

4. Undergo regular security audits.

Performing regular security audits can help ensure a safe and reliable payment processing system for your business.

These audits help identify any vulnerabilities that your system may have from potential threats. They also ensure you keep up to date with relevant data protection law so that your business can stay compliant.

Getting started with payment processing.

If you’re preparing to accept credit and debit card payments for your business or looking to update your payment process, Adobe Commerce is here to help.

A unified platform for payment processing, Commerce is a flexible, efficient way for businesses of all sizes to handle almost any transaction. Perhaps most importantly, Commerce keeps consumer data safe by complying with the latest in encryption and data security standards.

Learn more about how Adobe Commerce can help you make sure your business is ready to accept a variety of payment types.

Recommended for you

https://business.adobe.com/fragments/resources/cards/thank-you-collections/commerce