The type of payment processor you choose should depend on your sales volume, where your transactions take place, and the products or services you offer.

Some payment processors are better suited to handling certain types of transactions, such as mobile payments. Others offer capabilities that are necessary for specific businesses; for example, allowing your customers to enter their credit card numbers manually.

Think about the steps your customers need to take to complete a purchase and then determine the features you need from your payment processor.

1. Review your pricing plans.

The right payment processor should also be cost-effective. The cost to process each payment is small but can add up, especially if your business deals with many purchases each day. When evaluating payment processors for your business, consider which fee structure is the best deal. The right pricing model for you will depend on how you operate.

- If you’re a small brick-and-mortar business that occasionally sells items online, a tiered pricing structure can get you the lowest rates associated with in-person sales.

- If you’re a large business with a profitable ecommerce store, an interchange-plus pricing scheme could be a cost-effective solution.

You’ll also want to determine if a payment processor will charge fees for your subscription, or any equipment provided.

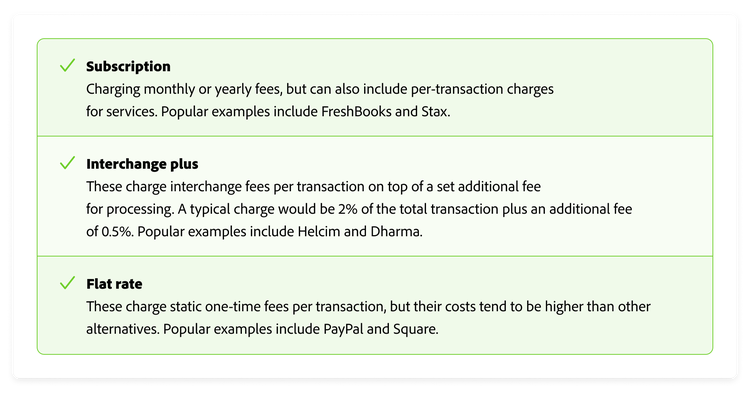

Interchange-plus.

The plus in interchange-plus refers to an additional fee that payment processors charge on top of the interchange fee. The additional fee covers the payment processor’s operations costs and provides them with a profit.

This amount is based on a fixed set of rates that may be applied to a transaction depending on the circumstances. The time the customer made the purchase, the card that was used, and whether the transaction was automated or not, are a few relevant factors. Premium credit cards are also typically more expensive to process than less exclusive ones.

Interchange fees are generally 1% to 3% of the overall transaction price. They also include a set dollar amount in cents for each transaction. The amount your business will pay for each transaction will vary with the interchange rate.

Flat-rate.

Flat-rate processing blends the variable interchange rate into one flat fee for all transactions. A flat-rate fee structure might add 2% of the purchase price plus an additional $0.10. Some businesses prefer flat-rate processing because it makes the fee easier to predict and simplifies revenue forecasting.

This simplified take on payment processing fees is ideal for smaller businesses and startups, which may not have the resources to apply a different interchange rate to every transaction. The downside is you typically won’t get the best possible rate for each type of debit or credit card payment you process, compared to an interchange-plus fee structure.

Tiered.

Tiered pricing, also known as bundled pricing, charges a fixed amount per transaction on different types of purchases. All transactions are classified into three tiers according to their risk — qualified, mid-qualified, and non-qualified — and assigned a corresponding fee.

Under a tiered payment processing system, an in-person debit card purchase may be categorized as a qualified transaction. This is a safe transaction that might warrant a processing fee as low as 1% of the total transaction plus $0.10.

However, a riskier online credit card purchase might be considered a non-qualified purchase. In this scenario, your business could be charged 3% of the total transaction fee plus $0.15.

2. Factor in the fees.

Fees can vary depending on the provider and the type of transactions you process.

Common charges to keep in mind include gateway fees for using a payment gateway, currency conversion fees for international transactions, and chargeback fees if a customer disputes a payment. Some processors also charge flat rates, while others have percentage-based fees.

3. Consider where you sell.

How and where you sell can have an impact on the fees you pay for payment processing.

If you have a physical store, in-person transactions using physical card terminals often have lower fees because they’re considered lower risk. On the other hand, digital online payments may have higher fees due to the high risk of online fraud and chargebacks.